The Utah affordability framework

Affordability is three overlapping numbers. First, the loan amount a Utah lender will approve based on your credit, income, and debt-to-income (DTI) ratio. Second, the monthly payment your household can actually absorb without starving retirement contributions, emergency savings, and normal life. Third, the all-in cost of owning a specific Utah home — a number that includes taxes, insurance, HOA dues, utilities, and a maintenance reserve.

Buyers who focus only on the first number end up house-poor. Buyers who only budget the second sometimes leave real affordability on the table. The framework below lines up all three so you make one decision, not three.

DTI: what lenders will approve

Debt-to-income ratio is the mechanical filter every lender uses. Front-end DTI is your proposed housing payment divided by gross monthly income. Back-end DTI adds in every other monthly debt — car payments, student loans, minimum credit-card payments, child support. The classic 28/36 guideline says keep front-end under 28% and back-end under 36%. In practice:

- Conventional loans usually cap back-end DTI around 45%, occasionally 50% with strong compensating factors.

- FHA loans stretch to roughly 56.9% back-end with automated underwriting approval.

- VA loans use a residual-income test — how much cash is left after all debts — alongside DTI.

- USDA loans generally target 41% back-end DTI.

Approval is not permission. Just because an underwriter will approve you at 50% DTI doesn't mean you should live there. Anchor your target at 36% and treat anything above as a deliberate stretch.

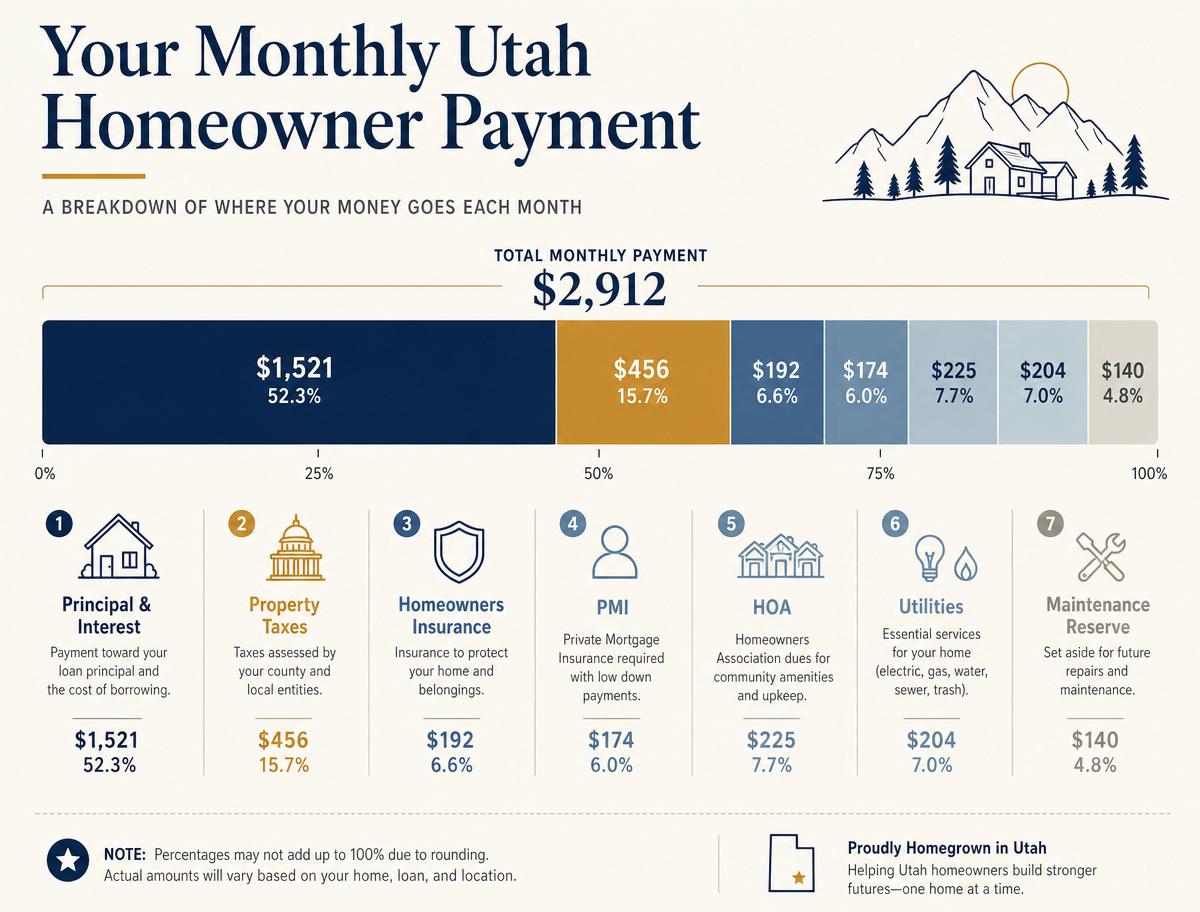

What actually goes into a Utah monthly payment

The mortgage payment is the smallest line item most buyers pay attention to and the biggest one they underestimate. Every Utah homeowner pays:

- Principal & interest — the "P&I" the calculators show.

- Property taxes — Utah's statewide effective rate averages around 0.55% of assessed value, one of the lowest in the country. Verify the parcel-level rate; individual taxing districts vary.

- Homeowners insurance — typically $80–$180/month depending on home value, roof age, and wildfire exposure.

- PMI or MIP — required on conventional loans under 20% down (drops off automatically at 78% LTV) and on all FHA loans.

- HOA dues — common in Utah master-planned communities and townhome projects; often $30–$300/month.

- Utilities — Utah gas/electric/water combined typically runs $180–$300/month.

- Maintenance reserve — budget 1–3% of the home's value per year for repairs, roof cycles, water heaters, and HVAC.

A worked Utah example — Emily and Josh

Emily and Josh are a two-income Utah County household. Combined gross income is $9,500/month. They have a $420 car payment and $180 in student loans. They've saved $22,000 and want to know what house they can afford.

A 36% back-end DTI puts their maximum total monthly debt at $3,420. Subtract the $600 in existing debt and they have $2,820 to spend on housing. Using a 6.75% 30-year fixed rate, 3.5% down FHA, and Utah's ~0.55% property tax rate, that budget supports a home in the $395,000–$415,000 range once taxes, insurance, PMI, and a small HOA are baked in.

A Utah DPA program that covers their 3.5% down payment would move their out-of-pocket from ~$14,000 to closing costs only (~$8,000), preserving cash reserves without changing their monthly payment. That's the difference between "we can barely close" and "we can close and still sleep."

Stress-test before you offer

- Model the payment at your rate + 1%. If it breaks the budget, you're already over-leveraged.

- Add a $200 line for utilities you don't currently pay (yard maintenance, water, snow removal).

- Assume property taxes rise 2–3% annually.

- Keep at least 3 months of the new PITI in reserve after closing.

The one number you actually need

Pick the monthly payment you can live with for the next five years. Everything else is math. Take that number into the Utah Home Affordability Calculator to convert it into a defensible home price, then bring it into a conversation with a Utah mortgage banker who can factor in DPA, program eligibility, and current rate sheets.