The Utah FHA loan, explained end to end.

Who may qualify, what credit really means on an FHA file, down payment and gift funds, mortgage insurance, seller credits, the FHA appraisal, and how FHA compares with Conventional and VA — in one place.

An FHA loan is a mortgage insured by the Federal Housing Administration and issued by an approved private lender. It may provide a lower-down-payment option and flexible qualification standards for eligible borrowers purchasing a primary residence. FHA does not lend the money and does not approve your loan — approval depends on credit, income, assets, debts, property eligibility, underwriting, and individual lender requirements.

FHA is more flexible on credit than some programs, but the file still has to qualify — score, payment history, debt-to-income, and documented funds are all reviewed. Credit and Mortgage Readiness →

Start here

Seven steps, in order. Each one has a different job.

The short entry-level overview — whether FHA is worth exploring, lower-down-payment options, and flexible qualification.

Every FHA task in order: preparation, preapproval, offer, appraisal, processing, and closing day.

The full educational guide: qualification, mortgage insurance, gift funds, appraisal, comparisons, refinancing, myths, and a glossary.

Model income, debts, and the full monthly payment, then compare FHA against Conventional, VA, and USDA.

A short self-assessment of credit, documentation, funds, and timing before you apply.

Side-by-side program structure so the choice is based on total cost, not just the rate.

Bring your checklist and questions. Educational, no obligation.

The Utah FHA Loan Consumer Guide

Learn how FHA financing works, who qualifies, mortgage insurance, down payment requirements, refinancing, buying your first home, and how to decide whether FHA financing is right for you.

New to FHA? Start with the Starter Kit

The FHA Loan Starter Kit is the concise entry point for first-time and repeat buyers who may need a lower down payment or more flexible qualification. It helps you decide whether FHA is worth exploring before you commit the time to the full Consumer Guide.

The Utah FHA process, start to finish

1. Review financial readiness

Look at income stability, savings, existing debt, and how a housing payment would fit your budget before applying. Preparation, not perfection, is what moves an FHA file forward.

2. Check your credit

Pull your reports, confirm the information is accurate, and review payment history. Credit score is one factor among several, and lender requirements may differ from FHA program guidance.

3. Estimate a comfortable payment

Model the full payment — principal, interest, property taxes, homeowners insurance, mortgage insurance, and any HOA — rather than principal and interest alone.

4. Review income and employment

Underwriting looks at the stability and documentation of income, not just the amount. Self-employment, commission, bonus, and part-time income are documented differently.

5. Review debts and debt-to-income

Monthly obligations reported on credit, including student loans, are weighed against income. DTI is one of the most common reasons an otherwise strong file needs restructuring.

6. Determine available funds

Identify the funds available for down payment, closing costs, prepaid items, and reserves, and where they are sourced and documented.

7. Explore gift funds and assistance

Gift funds from permitted sources and down-payment assistance programs may be options. Both require documentation, and program availability and terms vary.

8. Compare FHA with other programs

Compare FHA against Conventional, VA if eligible, and USDA where applicable — on total monthly payment, cash to close, mortgage insurance, and long-term cost.

9. Obtain preapproval

A full preapproval reviews credit, income, and assets. In Utah's market, a documented preapproval materially strengthens an offer.

10. Find an eligible primary residence

FHA financing is for a home you intend to occupy as a primary residence. Single-family homes, eligible condominium projects, and certain two-to-four-unit properties may qualify.

11. Make an offer

Negotiate price, timelines, and any seller contributions. Seller credits may reduce eligible buyer costs, subject to FHA and lender limits and to what the seller agrees to.

12. Complete the FHA appraisal

An FHA-assigned appraiser establishes value and reviews the property against FHA minimum property standards for safety, security, and soundness. It is not a substitute for a home inspection.

13. Complete underwriting

Underwriting verifies income, assets, credit, the appraisal, and title. Conditions are normal. Avoid new credit, large purchases, and job changes during this window.

14. Review the Closing Disclosure

Compare final figures against your Loan Estimate and your checklist, and ask about anything that changed before you sign.

15. Close and become a homeowner

After closing, keep documentation, track your mortgage insurance and escrow, and revisit refinancing only when the numbers and your goals actually support it.

What credit score do you actually need for FHA?

FHA program guidance and individual lender requirements are not always identical, and a specific score does not guarantee approval. Payment history, debt-to-income, income stability, assets, reserves, and recent credit events are all reviewed together — and some files are reviewed through manual underwriting.

FHA mortgage insurance (MIP), explained

Why it exists

FHA mortgage insurance protects the lender against loss. That protection is what allows approved lenders to extend FHA financing with a lower down payment and more flexible qualification.

Upfront and annual components

FHA mortgage insurance has an upfront premium charged at origination — commonly financed into the loan amount — and an annual premium.

How annual MIP is collected

The annual premium is generally collected in monthly installments as part of the mortgage payment, alongside principal, interest, taxes, and homeowners insurance.

MIP is not homeowners insurance

Homeowners insurance protects you and your property. Mortgage insurance protects the lender. They are separate line items with separate purposes.

MIP is not conventional PMI

Conventional PMI and FHA MIP are different programs with different structures, pricing, and removal rules. Do not assume what applies to one applies to the other.

How long it lasts

Duration depends on the loan structure and the rules applicable to that loan. It is not accurate to say MIP always disappears, or that it never does.

Refinancing is an option, not a guarantee

Refinancing into another program may be one future path to change mortgage insurance, but it depends on equity, credit, rate environment, and cost. It is not automatically beneficial.

Evaluate it in context

Mortgage insurance should be weighed with total monthly payment, cash to close, rate, how long you expect to keep the home, and your long-term goals — not in isolation.

FHA gift funds

- • Gift funds from permitted sources may be used toward eligible costs.

- • Documentation is required — a gift letter alone is usually not enough.

- • Gift money must not be disguised borrowed funds.

- • The donor and the transfer of funds may need to be verified.

- • Your lender determines what documentation is acceptable for your file.

FHA seller credits

- • Seller contributions may reduce certain permitted buyer costs.

- • They do not automatically replace all required borrower funds.

- • Concessions must comply with applicable FHA and lender rules and limits.

- • Purchase price and the appraised value still matter to the transaction.

- • Credits work best when structured around the buyer's actual costs.

FHA topics, explained

What an FHA loan is

A mortgage insured by the Federal Housing Administration and issued by an approved private lender. FHA does not lend the money; the insurance is what allows approved lenders to offer more flexible terms to eligible borrowers.

Who may qualify

Eligibility depends on credit, income, assets, debts, the property, FHA guidance, underwriting, and lender requirements. FHA is not limited to low-income borrowers and has no income cap.

First-time and repeat buyers

FHA financing is not restricted to first-time buyers. Repeat buyers purchasing a primary residence may also use it, subject to occupancy rules and underwriting.

Credit-score considerations

FHA publishes program guidance, and individual lenders apply their own requirements on top of it. A specific score does not guarantee approval, and score is reviewed alongside payment history, debt, income, and reserves.

Lender overlays

An overlay is a lender requirement stricter than FHA program guidance. Two lenders can review the same borrower and reach different conclusions because of overlays.

Down-payment requirements

FHA is known for a lower minimum down payment than many conventional options. The required amount depends on program guidance and the borrower's qualification profile at the time of application.

Gift funds

Gift funds from permitted sources may be used toward eligible costs. Documentation is required, the donor and transfer may need verification, and gift money must not be disguised borrowed funds.

Down-payment assistance

Utah Housing Corporation and various county, city, and grant programs may layer with FHA financing. Eligibility, funding availability, and repayment terms vary by program and change over time.

Debt-to-income ratio

DTI compares monthly obligations to gross monthly income. FHA underwriting can be more flexible than some programs, but the allowable ratio depends on compensating factors, automated findings, and lender guidelines.

Income and employment

Underwriting reviews documented, stable income. How income is calculated matters more than the headline figure, particularly for self-employed, commissioned, and variable-income borrowers.

Mortgage Insurance Premium

FHA loans carry mortgage insurance that protects the lender against loss. It exists so approved lenders can extend FHA financing under flexible terms. See the MIP section below for how the upfront and annual pieces work.

Seller contributions and credits

Sellers may agree to contribute toward eligible buyer costs within FHA and lender limits. Contributions are negotiated, not guaranteed, and do not automatically replace all required borrower funds.

Closing costs and cash to close

A lower down payment does not mean no cash. Earnest money, closing costs, prepaid taxes and insurance, and the upfront mortgage insurance premium if not financed all factor into total cash to close.

The FHA appraisal

An FHA appraisal estimates value and confirms the property meets FHA minimum property standards. Health, safety, and structural issues flagged by the appraiser typically must be addressed before closing.

Condominiums

A condominium may be eligible when the project or the individual unit meets FHA requirements. Confirm eligibility before writing an offer on a condo.

Two-to-four-unit properties

Certain two-to-four-unit properties may be eligible when the borrower occupies one unit as a primary residence, subject to FHA rules, reserves, and underwriting.

Manufactured and new homes

Manufactured homes have additional foundation and property requirements. New construction in Utah County and Washington County typically appraises without difficulty, but documentation requirements differ.

FHA vs. Conventional

FHA can be more accommodating on credit and down payment; conventional can be less expensive over time for borrowers with stronger credit and more equity. Compare total monthly cost and cash required, not just the rate.

FHA vs. VA

For eligible veterans and service members, VA financing generally has no required down payment within entitlement and no monthly mortgage insurance. When VA eligibility exists, both should be compared before choosing.

FHA Streamline Refinance

A streamlined option for refinancing an existing FHA loan into a new FHA loan with reduced documentation in some circumstances. Eligibility and benefit tests apply.

FHA cash-out refinance

An option for accessing equity, subject to loan-to-value limits, credit, occupancy, seasoning requirements, and underwriting. Cost and long-term impact should be evaluated, not assumed.

FHA 203(k)

Renovation financing that combines the purchase and eligible repair or improvement costs into a single FHA loan — useful for older Utah homes in Ogden, Provo, and parts of Salt Lake County.

FHA vs. Conventional vs. VA

General program structure only. Individual results depend on eligibility, credit, the property, and lender guidelines.

| Feature | FHA | Conventional | VA |

|---|---|---|---|

| Insurer or guarantor | Insured by FHA; issued by an approved private lender | Not government-insured; follows Fannie Mae / Freddie Mac guidelines | Partially guaranteed by VA; issued by a private lender |

| Down payment | Lower minimum than many conventional options, subject to qualification | As low as 3% for some borrowers; more options at 5%–20%+ | No required down payment within entitlement for eligible borrowers |

| Mortgage insurance | Upfront MIP plus annual MIP collected monthly | PMI when equity is below a threshold; generally removable | No monthly mortgage insurance; one-time funding fee unless exempt |

| Credit flexibility | Generally more accommodating, subject to lender requirements | Typically requires stronger credit for best pricing | No published universal minimum; lenders set requirements |

| Occupancy | Primary residence | Primary, second home, or investment | Primary residence |

| Renovation option | 203(k) renovation financing available | HomeStyle and similar renovation products | Limited renovation options |

| Who it often fits | Buyers with lower down payment or more complex credit | Buyers with stronger credit and more equity | Eligible veterans, service members, and certain surviving spouses |

FHA planning worksheets

Free, printable, and educational.

Utah FHA Home Buyer Checklist

Every FHA task in order — preparation, preapproval, home search, appraisal, underwriting, and closing day.

Utah Home Affordability Worksheet

Map your income, debts, and reserves to a comfortable Utah home price.

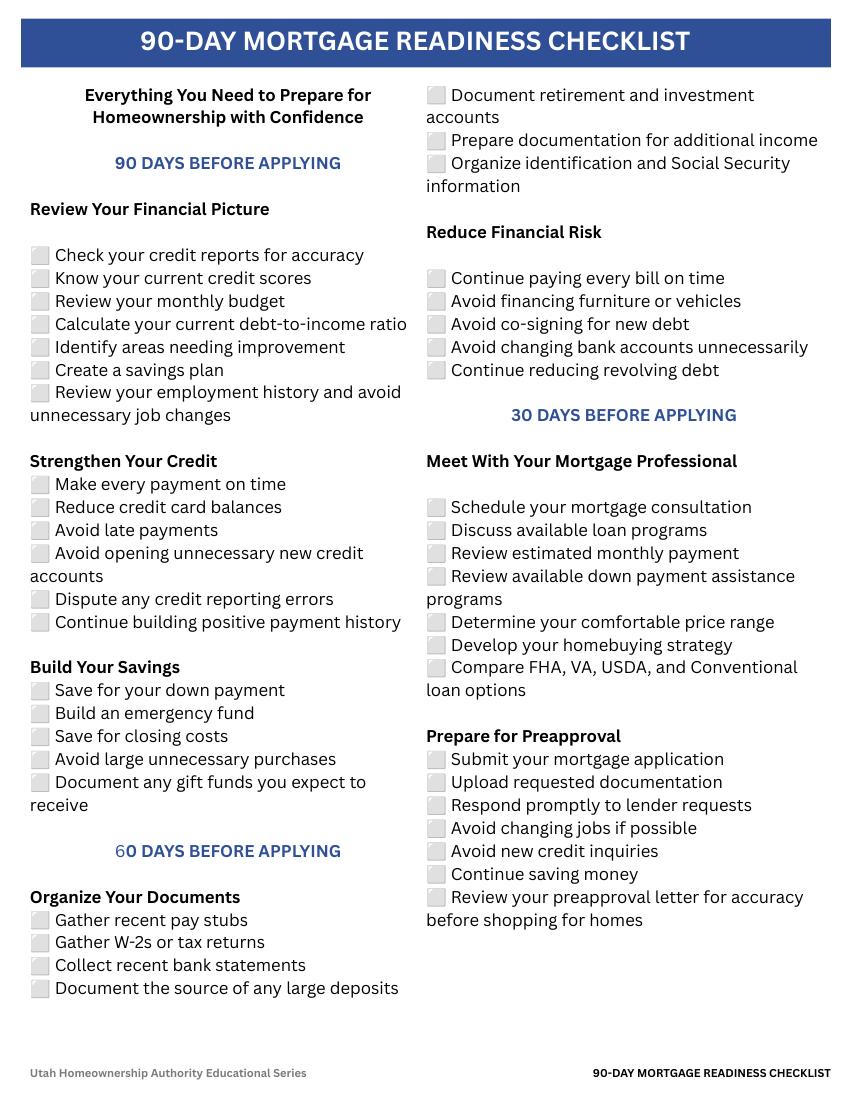

The 90-Day Utah Mortgage Readiness Checklist

A month-by-month plan to get credit, cash, and documents mortgage-ready before you write an offer in Utah.

The Utah FHA Home Buyer Checklist is FHA-specific and intentionally separate from the general First-Time Home Buyer Checklist and the 90-Day Mortgage Readiness Checklist.

Run your numbers and go deeper

Income, debts, and program comparison including FHA.

Principal, interest, taxes, insurance, and HOA.

Buyer costs, prepaids, credits, and cash to close.

The full first-time buyer path in Utah.

First thought to keys in hand.

Utah programs that may layer with FHA.

Compare FHA with conventional financing.

If you may be eligible, compare before choosing FHA.

Zero-down option for eligible rural Utah properties.

A real part of your monthly payment.

Different from mortgage insurance — both matter.

Begin the FHA preapproval process.

FHA videos by topic

Every video below is in the Video Library with a thumbnail, description, and captions available on YouTube.

FHA Basics

A short overview of FHA financing — a mortgage insured by the Federal Housing Administration and issued by an approved private lender, which may offer a lower down payment and more flexible qualification standards for eligible buyers of a primary residence.

Tres Miller busts three of the most common mortgage myths Utah homebuyers still believe — and shows what the truth means for your down payment, credit, and offer.

How Utah buyers who assume they can't afford a home often qualify with the right loan program, down payment assistance, or credit strategy.

Credit and Qualification

How credit is evaluated on an FHA file — why FHA program guidance and individual lender requirements are not always identical, and why a credit score alone does not determine approval.

How debt-to-income ratio is calculated and why lenders use it as one factor when evaluating a borrower's ability to qualify for a mortgage.

How credit scores can affect mortgage qualification, and why minimum credit requirements can vary by loan program, lender guidelines, and individual borrower circumstances.

Cash Needed

The types of cash a homebuyer may need when purchasing a home — down payment, closing costs, prepaid expenses, and other transaction-related costs.

How seller contributions may help cover eligible buyer closing costs on an FHA purchase, and why concessions are negotiated, limited by program rules, and do not automatically replace all required borrower funds.

How seller-paid closing costs — sometimes called seller concessions — may help cover eligible buyer closing expenses, subject to loan-program and transaction limits.

How down payment assistance programs generally work, who may qualify, and why program requirements, funding availability, and repayment terms can vary.

Comparisons and Strategy

Key differences between FHA and conventional mortgage financing — general qualification considerations, down payment options, mortgage insurance, and borrower profiles.

The key factors that influence home affordability — income, debts, available cash, and the monthly payment a buyer is comfortable managing.

Financial and credit changes that may affect a mortgage application before closing — new debt, employment changes, large purchases, and unexplained financial activity.

FHA questions Utah buyers ask

What is an FHA loan?

An FHA loan is a mortgage insured by the Federal Housing Administration and issued by an approved private lender. It may provide a lower-down-payment option and more flexible qualification standards for eligible borrowers purchasing a primary residence. FHA is not the lender.

What credit score do I need for an FHA loan in Utah?

There is no single answer. FHA publishes program guidance, and individual lenders apply their own requirements on top of it. Credit score is one factor reviewed alongside payment history, debt-to-income, income stability, assets, reserves, and recent credit events. A specific score does not guarantee approval.

Does FHA guarantee approval at a particular credit score?

No. Meeting a score threshold does not by itself produce an approval. Approval depends on the full file — credit, income, assets, debts, the property, FHA guidance, underwriting, and lender requirements.

How much down payment do I need for an FHA loan?

FHA is known for allowing a lower minimum down payment than many conventional options. The amount required for your file depends on current program guidance and your qualification profile. Gift funds and down-payment assistance may also be options.

Can I use gift funds for an FHA down payment?

Gift funds from permitted sources may be used toward eligible costs. Documentation is required, the donor and the transfer may need to be verified, and the funds must be a true gift rather than disguised borrowed money. Your lender determines acceptable documentation.

Can the seller pay my closing costs on an FHA loan?

A seller may agree to contribute toward eligible buyer costs within FHA and lender limits. Seller contributions are negotiated, not automatic, and they do not necessarily replace all required borrower funds. The purchase price and the appraisal still matter.

What is FHA mortgage insurance?

FHA mortgage insurance protects the lender against loss and is what allows approved lenders to offer FHA terms. It has an upfront component and an annual component, and it is different from homeowners insurance and from conventional PMI.

Does FHA mortgage insurance ever end?

It depends. How long annual MIP stays on a loan depends on the loan structure and the rules applicable to that loan. Refinancing into another program may be one future option, but it is not automatically beneficial and should be evaluated against payment, cash to close, rate, and long-term goals.

What is upfront MIP?

The upfront mortgage insurance premium is charged at loan origination. It is commonly financed into the loan amount rather than paid in cash at closing, which affects the loan balance.

What is annual MIP?

The annual mortgage insurance premium is generally collected in monthly installments as part of the mortgage payment. It is separate from homeowners insurance and from property taxes.

How is FHA different from a conventional loan?

FHA can be more accommodating on credit and down payment and carries FHA mortgage insurance. Conventional financing may cost less over time for borrowers with stronger credit and more equity, and its PMI can generally be removed at certain equity thresholds. Compare total cost, not just the rate.

How is FHA different from a VA loan?

For eligible veterans, service members, and certain surviving spouses, VA financing generally requires no down payment within entitlement and carries no monthly mortgage insurance. If you may be VA-eligible, compare both before choosing FHA.

Can repeat buyers use FHA financing?

Yes. FHA is not limited to first-time buyers. Repeat buyers purchasing a primary residence may also use FHA financing, subject to occupancy rules and underwriting.

Is FHA only for low-income buyers?

No. FHA has no income limit. It is often used by buyers who want a lower down payment or need more flexible qualification, regardless of income level.

Can I use down-payment assistance with an FHA loan?

Down-payment assistance may layer with FHA financing in many cases. Program eligibility, funding availability, structure, and repayment terms vary by program and change over time.

How does debt-to-income affect FHA approval?

DTI compares your monthly obligations to gross monthly income and is a central underwriting factor. FHA can be more flexible than some programs, but the allowable ratio depends on compensating factors, automated findings, and lender guidelines.

How are student loans counted on an FHA loan?

Student loans are generally included in the debt calculation even when payments are deferred or on an income-driven plan. How the monthly figure is calculated follows FHA guidance and lender interpretation, so ask before assuming a deferred loan is excluded.

What is FHA manual underwriting?

When an automated underwriting system does not return an acceptable finding, a file may be reviewed manually by an underwriter. Manual underwriting applies additional scrutiny and may require compensating factors such as reserves, a lower DTI, or a stronger payment history.

What does an FHA appraiser inspect?

An FHA appraiser estimates market value and reviews the property against FHA minimum property standards for safety, security, and soundness. Common Utah flag items include chipped paint on older homes, missing handrails, roof condition, and water intrusion. An appraisal is not a home inspection.

Can I buy a condominium with an FHA loan?

A condominium may be eligible when the project or the individual unit meets FHA requirements. Confirm eligibility before writing an offer, because approval status varies by project.

Can I buy a duplex with an FHA loan?

Certain two-to-four-unit properties may be eligible when you occupy one unit as your primary residence, subject to FHA rules, reserve requirements, and underwriting.

Can I buy a manufactured home with an FHA loan?

Manufactured homes may be eligible, but they carry additional foundation, titling, and property requirements. Confirm eligibility for the specific home early in the process.

Can I use FHA financing for an investment property?

FHA financing is intended for a primary residence you will occupy. A two-to-four-unit property where you occupy one unit may be an option, but a pure non-owner-occupied investment purchase is not.

What is an FHA 203(k) loan?

A 203(k) combines the purchase price and eligible renovation costs into a single FHA loan. It is often used on older Utah homes that need repairs an FHA appraiser would otherwise flag.

What is an FHA Streamline Refinance?

A streamlined path to refinance an existing FHA loan into a new FHA loan with reduced documentation in some circumstances. Eligibility requirements and net-benefit tests apply, and it is not automatically the right move.

How much cash will I need at closing on an FHA purchase?

Total cash to close typically includes the down payment, closing costs, prepaid property taxes and homeowners insurance, and the upfront mortgage insurance premium if it is not financed — less earnest money already paid and any seller or lender credits.

What should I do first?

Read the FHA Loan Starter Kit, complete the Utah FHA Home Buyer Checklist, then read the Utah FHA Loan Consumer Guide and run the Home Affordability Calculator. Those four steps cover preparation before you speak with a lender.

Is Utah Homeownership Authority part of FHA or HUD?

No. Utah Homeownership Authority is a private educational and mortgage resource. It is not a government agency and is not affiliated with, endorsed by, or acting on behalf of HUD or FHA. Official program information is published by HUD at hud.gov.

Wondering whether FHA is your best option?

Bring your checklist and your questions. Tres will walk through qualification factors, payment, and cash to close, and compare FHA against the other programs you may qualify for — educational, no obligation.